Debt Relief Options Used by Many Americans

Learn About Debt-Free Solutions Today!

Your Debt Resource is a free informational and matching service designed to help consumers explore debt relief solutions through qualified providers.

No Credit Check

No Obligation

2-Minute Quiz

As Featured In

Forbes

CNBC

Bloomberg

USA Today

The Wall Street Journal

WE UNDERSTAND

Explore Our Debt

Information & Options

Learn more about commonly explored debt relief approaches, educational resources, and services that may help consumers better understand their available options.

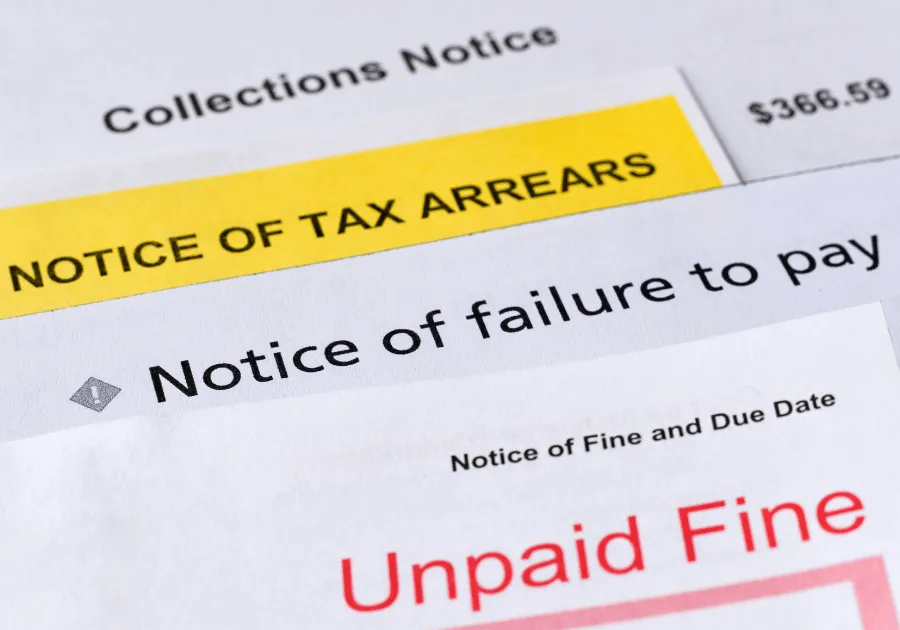

Concerned about collection calls?

Some debt relief programs may help consumers explore structured repayment or settlement options through third-party providers.

Managing high credit card balances?

Explore educational resources and debt relief options that consumers commonly research when looking for ways to manage unsecured debt.

Looking for financial guidance?

Learning about available debt relief and budgeting options may help consumers make more informed financial decisions.

A RE You Can Rely On

Real People.

Real Support. Real Results.

Your Debt Resource connects consumers with third-party professionals and educational resources related to debt relief and debt settlement options.

You don’t have to research everything alone. We help simplify the process of exploring available options and connecting with experienced providers.

No Credit Check

Confidential Process

SIMPLE PROCESS

Explore Debt Relief Options in 3 Simple Steps

Learn more about available debt relief and settlement options through a short informational process.

Answer a Few Questions

Complete a short, confidential questionnaire about your financial situation.

Review Available Options

Learn about debt relief approaches and services that may fit your circumstances.

Speak with an Expert

Get connected with a third-party specialist for additional information.

COMPREHENSIVE DEBT SOLUTIONS

We can help you address a wide range of debt types

Credit Card Debt

High-interest revolving balances. Average balances of $10K+

Collections Accounts

Past-due unsecured balances

Unsecured Debt

Qualifying non-collateralized debt

Store Card Debt

Retail and revolving account balances

COMPREHENSIVE DEBT SOLUTIONS

Explore Debt Relief Options

Explore targeted solutions tailored to free you from financial burdens.

Credit Card Debt

Revolving balances with variable interest rates. Many consumers explore debt relief options when monthly payments become difficult to manage over time.

Collections Accounts

Past-due accounts that may have been transferred or sold to collection agencies. Consumers often research repayment and settlement options for these balances.

Unsecured Debt

Debt not backed by collateral, including certain credit accounts and qualifying balances. Program eligibility may vary based on debt type and amount.

Store Card Debt

Retail financing and revolving store accounts can accumulate over time, especially with multiple active balances and promotional interest terms.

REAL STORIES

A Life Transformed

“When I first came to YourDebtResource, I had over $45,000 in credit card debt. I was stuck making minimum payments and couldn’t see a way forward.

The specialist I was connected with helped reduce my debt by 52%, and now I’m on track to be completely debt-free within 18 months. For the first time in a long time, I feel hopeful about my future.”

Angela D.

Portland, OR — On track to be debt-free in 18 months

50,000+

PEOPLE HELPED

$1500M+

DEBT RESOLVED

47%

AVG. REDUCTION

4.9/5

CLIENT RATING

See What’s Possible

How much could you save?

When you’re dealing with debt, it can feel like there’s no way out. But many people are able to reduce what they owe by more than they expected.

On average, clients see savings of around 47% on their total debt. For example, a $10,000 balance could potentially be reduced by nearly half.

Your situation is unique, but with the right approach, real progress is possible. Take a quick, confidential quiz to explore what your potential savings might look like.

If you owe

$15,000

You could save

$7,050

If you owe

$30,000

You could save

$7,050

If you owe

$15,000

You could save

$7,050

Debt Relief Calculator

Example: $35,000 total debt

Your total debt

$35,000

Potential savings (47%)

-$16,450

You could pay

$18,550

That's $16,450 back in your pocket!

QUESTIONS & ANSWERS

Frequently Asked Questions

What types of debt may qualify for debt relief programs?

Some debt relief programs may apply to qualifying unsecured debts such as credit card balances, collections accounts, and certain store card balances. Eligibility varies depending on the provider, debt amount, and individual circumstances.

Is debt relief a good option for everyone?

Debt relief programs are not appropriate for every financial situation. Different consumers may benefit from different approaches depending on factors such as income, total debt, payment history, and financial goals. Exploring educational resources and speaking with a qualified provider may help consumers better understand available options.

How could debt relief programs affect my credit score?

Some debt relief and settlement programs may impact credit scores, especially if accounts become delinquent during the process. Outcomes vary by individual situation and program type. Consumers should carefully review potential risks, benefits, fees, and long-term financial considerations before enrolling in any program.

What are the costs associated with debt relief services?

The fees vary depending on the service and your debt situation. All costs are outlined during your initial consultation with your provider.

How long does the debt relief process typically take?

Program timelines vary significantly based on debt amount, creditor participation, and individual circumstances.

What makes Your Debt Resource different from other debt relief companies?

Your Debt Resource is a free informational and referral platform designed to help consumers learn about debt relief options and connect with third-party providers. We focus on educational content, simple online assessments, and helping consumers explore available solutions based on their financial situation.

Free 2-Minute Assessment

Start your journey today

Complete a short, confidential questionnaire to learn more about debt relief approaches and available resources through third-party providers.

Information is educational in nature and results vary based on individual circumstances.

100% Confidential

No Credit Check

Takes 2 Minutes

Important:

Your Debt Resource is a free informational service that may connect you with third-party debt relief providers. We are not a lender, creditor, or debt relief provider. We may receive compensation from partners for referrals. By submitting your information, you agree to be contacted by us and/or third-party providers. Results are not guaranteed and vary based on individual circumstances.

This site is not part of the Facebook™ website or Facebook™ Inc. and is not endorsed by Facebook™ in any way.

Contact Us

5629003522

123 Main ave